Key points

– The $A has been hit since September by the return of Trump, a hawkish pivot by the Fed versus the RBA and concerns about the outlook for iron ore prices.

– We doubt the fall is significant enough to boost inflation much and shouldn’t stop the RBA easing in February if underlying (or trimmed mean) inflation falls as expected.

– In any case, it’s now had a bit of a bounce from oversold levels as Trump refrained from Day One tariffs opting for government agencies to investigate unfair trade & tariffs and reportedly more of a negotiating approach.

– The $A could be stuck between $US0.60 and $US0.70, but with the risk skewed to the downside if Trump acts more aggressively on tariffs in the months ahead. Note, Trump still said in his inaugural speech that tariffs are coming.

Introduction

Currency markets are well known to be volatile – as there is no clear agreement on how to value them and they are vulnerable to international shocks and shifts in investor sentiment. Changes in the value of the $A are important as they impact Australia’s export competitiveness and the cost of imports, including that of overseas holidays. For investors they directly impact the value of international investments and indirectly impact the performance of domestic assets via the impact on competitiveness.

Unfortunately, currency forecasting is a bit of a mugs game to which John Kenneth Galbraith’s observation in relation to economic forecasters that there are “those who don’t know and those who don’t know that they don’t know” may apply. So, it should not be surprising the value of the $A continues to surprise. Six months ago, when the $A rose to $US0.67 we thought it would go higher for various reasons including that it was slightly undervalued and interest rate differentials looked likely to shift in favour of Australia. As it turns out it did go higher, rising above $0.69 in September. But then it fell sharply, recently reaching a low of $US0.615. This in turn has led to concern about a boost to inflation and the RBA being less able to cut interest rates and possibly having to raise rates. This note looks at what’s driven the fall, the outlook and its implications.

Why has the $A fallen since September?

The fall in the value of the $A reflects a combination of three things:

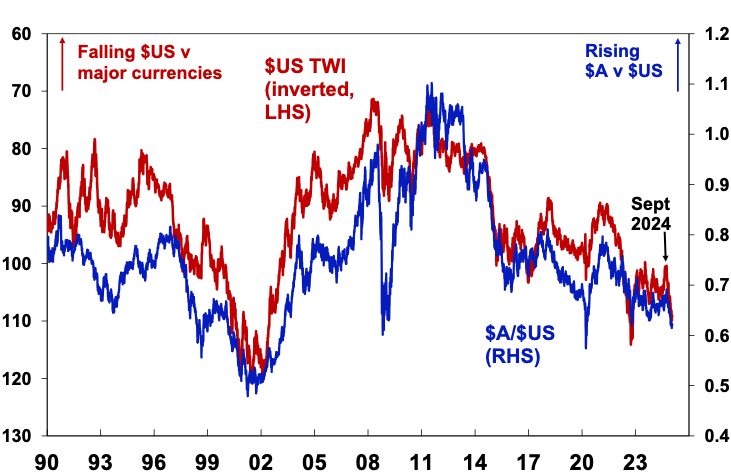

- The return of Trump – support for the Democrats peaked around late September/early October and so markets moved to price in the rising probability and then reality of his return to the presidency. Since his policies – tax cuts and deregulation which could boost US productivity, tax cuts which could add to the US budget deficit and result in tighter Fed policy, and tariffs – all imply a stronger US dollar this is what we have seen with the $US rising around 9% against a basket of major currencies from its September low.

The $US v major currencies & the $A

Source: Bloomberg, AMP

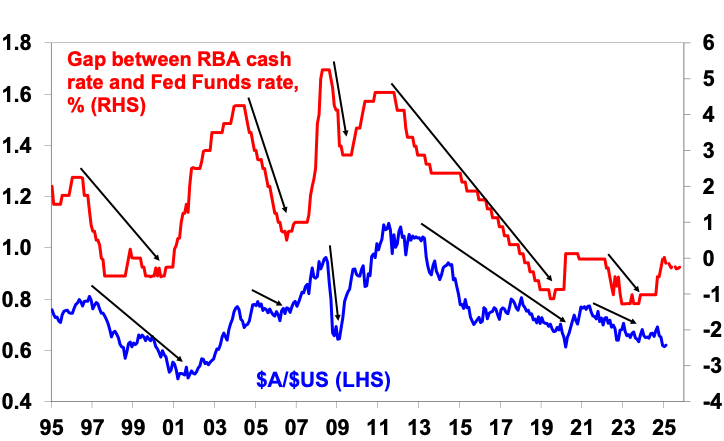

- A hawkish pivot by the Fed versus the RBA – whereas the Fed cut rates in December to 4.25-4.5% it signalled less cuts than previously expected through 2025 whereas confidence has grown that the RBA will start to cut rates. As a result, the interest rate gap between the Australia and the US is expected to deteriorate in contrast to previous expectations for an improvement. Historically the $A goes up when the Australian interest rates rise versus US rates and vice versa.

The interest rate gap between Aust & the US versus the $A

The dashed part of the rate gap line reflects money mkt expectations. Source: Bloomberg, AMP

- Finally, concerns about the outlook for the iron ore price, Australia’s biggest export, rose after disappointing stimulus announcements in China and fears that US tariffs on China could reduce demand for Australian commodities – that said iron ore prices and wider commodity price indexes are above their September lows suggesting commodities have not really been a major driver of the fall in the $A.

So, the fall since September is mainly a strong US dollar story rather than a week $A story as since September the $A fell around 10% but the $US rose around 9% as other major currencies also fell against the $US.

Will the fall add to inflation & hamper RBA rate cuts?

It’s not the RBA’s role to defend the $A or maintain it at a particular level -otherwise it would defeat the whole purpose of having a flexible exchange rate which is to provide a shock absorber to events that threaten our growth outlook – like less demand for our exports. But it’s fall will be of some concern to the RBA in terms of the risk that it poses to inflation as a fall in the value of the Australian dollar by boosting import prices could add to inflation. However, there are several reasons why the RBA is unlikely to be too concerned.

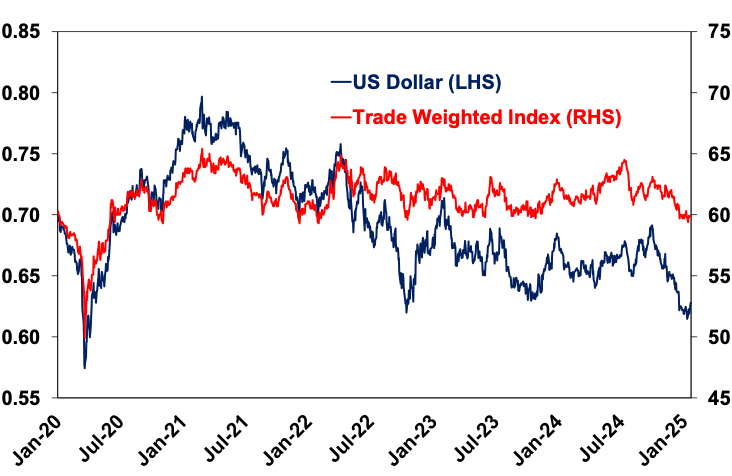

- Firstly, while the $A has had roughly a 10% fall from September against the $US, other countries’ currencies have also had sharp falls against the $US so the value of the $A on a trade weighted basis is only down by around 5% over the same period which is neither here nor there in terms of the impact on in inflation.

- Secondly, on a trade weighted basis the $A is in basically the same range it’s been in for the last four year now. And with President Trump holding off from Day One tariffs and opting instead for a US government review of them and a “more negotiating approach” with China (according to a Bloomberg report) the range appears to be holding with the $A bouncing slightly from oversold levels.

The Australian dollar, measured against…

Source: Bloomberg, AMP

- Thirdly, with consumer spending depressed it’s hard to see businesses being able to pass on higher import prices anyway – beyond higher petrol prices and international travel – without depressing demand.

So, it’s hard to see a significant boost to the inflation outlook from the fall in the Australian dollar so far and so the RBA shouldn’t be too concerned – albeit I have no doubt it will mention it in upcoming communications.

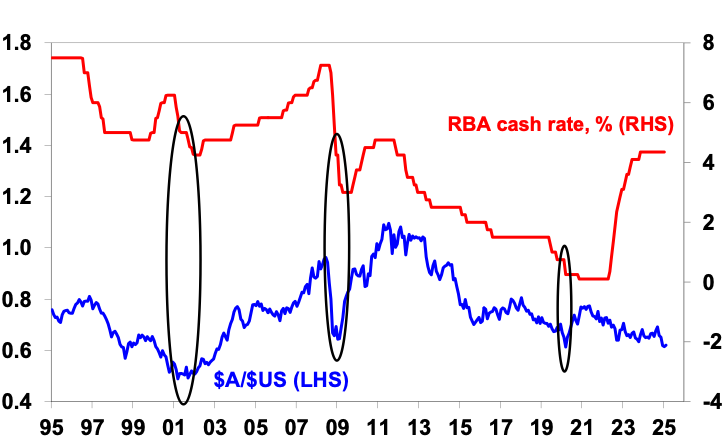

It’s worth noting that the $A plunged in 2001 (to $US0.48); 2008 (from $US0.98 to $US0.60 in 3 months) and in the pandemic (to $US0.57) and yet the RBA eased on each occasion with other factors dominating!

The RBA has eased several times when the $A fell sharply

Source: Bloomberg, AMP

In short, while the fall in the $A will concern the RBA we don’t see it as being enough to stop the RBA from cutting rates ahead. Ultimately, the rates decision next month will come down to December quarter inflation data to be released next week. If trimmed mean inflation comes in at 0.6%qoq or less as looks likely as against implied RBA expectations for a 0.7%qoq rise it will be very hard for the RBA not to cut in February.

Despite the slide there are several positives for the $A

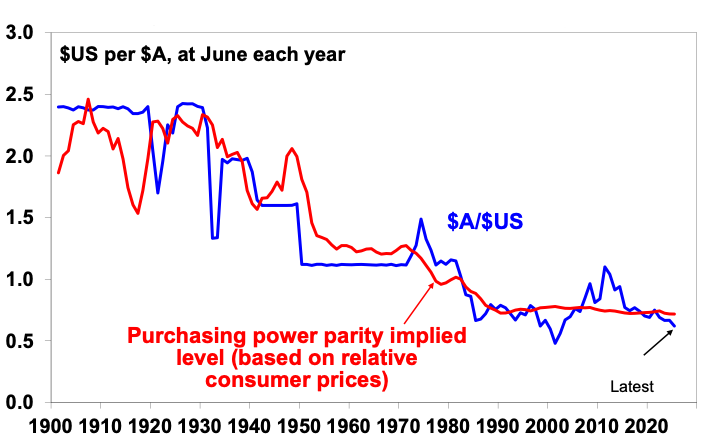

- Firstly, from a long-term perspective the $A remains cheap. The best guide to this is what is called purchasing power parity (PPP) according to which exchange rates should equalise the price of a basket of goods and services across countries (the red line in the next chart). If over time Australian prices and costs rise relative to the US, then the value of the $A should fall to maintain its real purchasing power. And vice versa if Australian prices fall versus the US. Consistent with this the $A tends to move in line with relative price differentials over the long-term. Right now, it’s cheap at around $US0.63 compared to fair value around $US0.72 on a purchasing power parity basis.

The $A is below fair values based on relative prices

Source: RBA, ABS, AMP

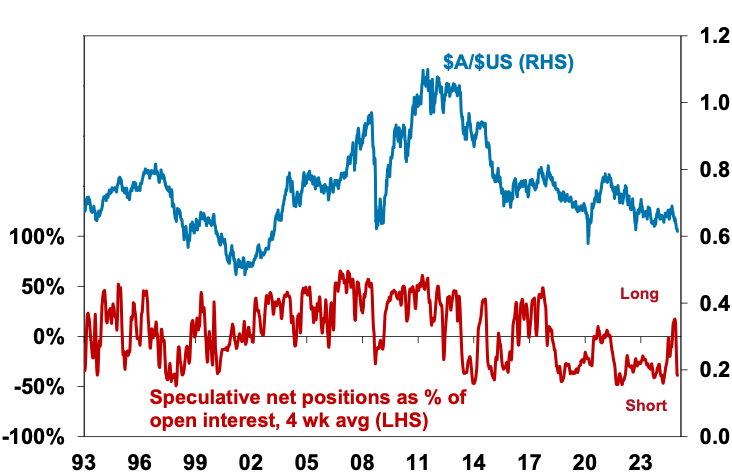

- Second, sentiment towards the $A is negative, reflected in short or underweight positions. Many of those who want to sell the $A may have already done so and Trump’s return may already be factored in, and this leaves it susceptible to a rally if there is any good news.

$A positioning is back to short

Source: Bloomberg, AMP

- Finally, commodity prices look to be embarking on a new super cycle. The key drivers are the trend to onshoring reflecting a desire to avoid a rerun of pandemic supply disruptions and increased nationalism, the demand for clean energy and increasing global defence spending all of which require new metal intensive investment compounded by global underinvestment in new commodity supply.

Where to from here?

In the short term the $A is bouncing from oversold levels (and the $US falling from overbought levels) as Trump’s return was largely factored and so far his bite has been less than his bark. Over the next 12 months it’s likely to be buffeted between changing views as to how much the Fed will cut relative to the RBA and how far Trump goes on tariffs (so far so good – but there is a way to go yet as Trump is still saying tariffs are coming) versus potential positives of undervaluation, negative sentiment and maybe more decisive stimulus in China. This could leave it stuck between $US0.60 and $US0.70, but with the risk skewed to the downside if Trump acts more aggressively on tariffs.

Implications for investors?

While the fall in the value of the $A will add to the cost of petrol and overseas travel (mostly to the US) and could constrain the RBA in cutting rates, although we don’t think this will be significant, there is a silver lining to the cloud in that the fall has boosted the value of (unhedged) international assets so it has enhanced returns in global shares. This highlights the benefits of having a well-diversified investment portfolio across both assets and also across currencies.

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.